Responses to article VoV #11 (2021)

Responses to article VoV #11 (2021)

Responses to article: 'Calculating with a low discount rate'

Note: Text in >>> italicized <<< by Gerard Filé

The responses are in a personal capacity and do not necessarily have to express the position of the own organization.

07 29 - Response from Gerard Filé

Ed, Martine, Nice article, certainly food for thought…

I am challenged by the said 300 years. This stimulates my imagination. I am curious what our ancestors thought about infrastructure in 1721 and what calculations they made with regard to roads and dikes they were working on (cart tracks, canals and seaweed dikes). Only 100 years later it was decided to dig the Noord-Hollandsch canal: to put it in perspective… I am also curious how the Coentunnel and the A8 will look in 300 years… (probably the waves of the North Sea are lapping 6 meters above it and the concrete has been swallowed up by the bottom of the sea. Peace will have returned to the swampy Dutch delta I fear, and those busy people must be smashing each other's heads elsewhere...).

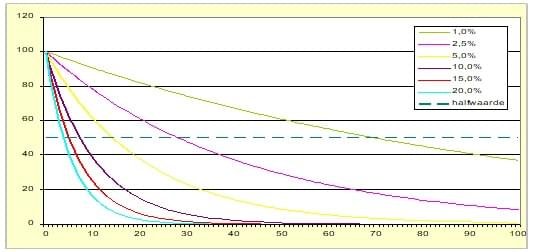

If the economic life is so short in practice, what's wrong with working with a higher discount rate? Why should the discount rate follow the market? In 5 years with a different economic wind you may need a higher percentage… Assuming that your infrastructure has to be profitable, I think it is justifiable to continue to calculate with, for example, 5% (half-value of money after 18 years and still at 70 years about 5% left.After 50 to 70 years it is usually pretty much 'used' and you still need another functionality, would be my proposition.) In the meantime you want to maintain meaningfully and not unnecessarily (re) to invest.

I think the calculation method should support that. I think it's strange to be blown away by the capital market. We should come up with something smarter for that. Would it be an idea to take the economic earning potential (social benefit) as a starting point and then use that to calculate what a meaningful discount rate is for investment and maintenance costs? (That's how they do it at factories, don't they?) Do the SCBAs offer any guidance?

07 29 - Answer from Martine van den Boomen to Gerard Filé

Dear Gerard,

Thank you for your stimulating response.

If I have understood you correctly, you argue that increasing the social discount rate does not require a different calculation method. That's right, but… that's outside the scope of our article. The social discount rate (economists) working group examines this discount rate every five years and issues advice. We have adopted that as a starting point. >>> Reaction Gerard Filé: The question is whether it is wise to accept this (tightening) precondition! <<<

We indeed assume a recurrence principle and explain that this is an estimate of future costs and benefits. You are absolutely right that objects/technological solutions change. However, we argue that the recurrence principle is closer to estimating future costs and benefits than looking no further than 100 years. So yes, we agree with you on this point but argue that the feature will continue to exist (in whatever form). >>> Gerard Filé response: If the method supports the goal, then it is of course okay. <<<

The EAC (and P-infinity) method also holds up with a high discount rate; because even then variants with different service lives will have to be compared with each other. But, certainly an interesting perspective you bring up. You could also write an article or opinion piece about this. It would also be interesting research for us.

Kind regards, Martine

07 29 - Reply from Rob Treiture to Gerard Filé .'s response

Dear Gerard,

Although your response is not directly addressed to me, I still feel compelled to respond as the instigator of the research that we from RWS are doing together with TU-Delft and which also prompted this article in VoV.

You can of course be very joking about the 300 years. Strangely enough, no one ever falls for a method such as EAC, which is recommended by many, because you only have to think about one life cycle. While, as stated in the article, this method has an infinite calculation, ie infinitely longer than 300 years. In this context, I miss a thought experiment about what dinosaurs should do with roads or dikes. >>> Gerard Filé response: Good to look for a better method. I don't want to cut these legs. It's about the method (and not the year). As a simple, practically oriented cost expert, images immediately arise at 300 years, I will not be the only one in that… <<<

RWS currently calculates at LCC with a fixed time horizon of 100 years. This was deliberately chosen at the time and for a number of reasons:

- Many of our newer assets have a design life of 100 years.

- It is usually relatively easy for a cost estimator to envision the required maintenance in 100 years (I immediately admit that we did not give enough thought to something as short cyclical as, for example, software at the time).

- At a discount rate of 3%, you make a methodical calculation error of a maximum of about 5% for 100 years, which we thought at the time was negligible in view of all other uncertainties.

A method like EAC may seem simpler at first glance, but it is not when you consider that the practice does not always consist of a continuous repetition of the exact same cycle. With a calculation over 100 years, discontinuities that are (and are known) in the near future are much easier to realize in the LCC calculation. For this reason, the EAC method was dropped at the time.

Now that we at the government are forced to calculate for LCC issues in the domain of the physical infrastructure with a discount rate of 1.6%, the methodical calculation error suddenly increases to about 20% with a horizon of 100 years. It is then not justifiable that this should be negligible in view of all other uncertainties. Hence the research into our LCC calculation method at low discount rates that we as RWS are now conducting together with TU-Delft. Here we look at alternative calculation methods as discussed in the article . >>> Gerard File's reaction: Enlightening! Good motivation of why this article now! <<<

A response to your comments.

- Why calculate in 100 years, 300 years, infinite years? We can't even look 10 years ahead! (my own interpretation of your initial comments)

LCC is a method of including expenses further in the future when making investment decisions. Where previously only the investment costs were considered, we now also look at the costs over the entire lifespan in order to avoid "cheap is expensive". >>> I think this is an important core value <<< This is recognized worldwide as good practice in asset management.

When costs occur at different points in time, the time value of money must be taken into account. We use a discount rate for this. In addition, scientific literature on LCC recommends an infinite calculation. Can we also reason this infinite calculation in a simple way? Yes, the function of most assets does not suddenly disappear at the end of the (technical) lifespan. Usually something new takes its place (that also applies to something like software, by the way). Is that always exactly the same? No, of course we can't predict the future, but assuming something is better than assuming nothing, because it's less likely that something will cease to exist. >>> Reaction Gerard File: Eens! Still, it is nice if you can validate these assumptions at all times and show that you contribute to the goal: being able to make a balanced decision with regard to investing and maintaining. <<< - If the economic life is so short in practice, what's wrong with working with a higher discount rate?

As I already indicated, the level of the discount rate at RWS / central government is not a free choice. The discount rate working group conducts a thorough investigation into this and comes up with a recommendation that has been adopted by the House of Representatives. The article does not address the question of what we think of this advice. >>> Gerard Filé response: A value engineer must also be able to discuss the scope (or in this case the basic rules) if it can be demonstrated that this does not make a good decision. <<< - In the meantime, you want to maintain meaningfully and not (re)invest unnecessarily. I think the calculation method should support that. I think it's strange to blow along with the capital market. We should come up with something smarter for that…

The current capital market indeed influences the current time value of money. Money is currently cheap for the central government, a low discount rate means that costs will weigh more heavily in the future. As a result, if we only reason from LCC, with a low discount rate, replacement is preferred rather than renovation. However, LCC is of course not the only weighting criterion in investment decisions. An aspect such as sustainability is also taken into account in addition to many more aspects . >>> Reaction Gerard File: Gluckily yes! This is also the gist of Ed's response in his afterword. <<< - Would it be an idea to take the economic earning potential (social benefit) as a starting point and then use that to calculate what a meaningful discount rate is for investment and maintenance costs? (That's how they do it at factories, don't they?) Do the SCBAs offer any guidance?

The discount rate working group has indeed looked at it from a social perspective. LCC is also part of a SCBA, in which social costs and benefits are taken into account. A SCBA is a heavy instrument with high costs and long lead times and is used to a limited extent. For smaller issues, Business Cases are drawn up at RWS, of which LCC is also a part.

(In the case of factories, social costs and benefits are usually not taken into account in investment decisions, this is more something for governments that serve the social interest.) >>> Gerard Filé response: What I actually meant is: a factory must pay for itself within X years . This translates into a risk premium/return requirement that partly dictates the level of the discount rate. Perhaps this return requirement (independent of the capital market) should be determined on the basis of quantified social/economic benefits. The infrastructure object must pay for itself within X years and that includes Y%… This consideration may be somewhat out of the context of the article and we may have to pay more attention to it later! <<<

I hope my response has given you some additional food for thought. >>> Gerard File's reaction: That worked Rob! To be continued! <<<

With kind regards,

Rob

30-07 - Gerard Filé's response to messages from Martine and Rob

Hi Rob (and Martine),

Thank you for your detailed answer/response! The subject is alive and good that attention is being paid to it. The context you provide in your answer may also add value to the article. This provides background information in the search that you are going through as a stakeholder. It might be interesting to use this in an introduction (with the answer to the 'why'…) at the risk of the article becoming too long….

Because I can't resist a few comments in your text ( >>> italicized <<< )

I don't know if we should do something about this email exchange right now. In any case, the article is provocative enough to provoke reactions (which is a compliment!) Perhaps there will be more reactions and we'll have to wait for that first. I am privileged to be able to respond (prematurely) now because Ed has framed me in the editors of VoV…. Every disadvantage has its advantage….

Regards, Gerard